Every business owner knows they need to maintain a consistent stream of new customers. They also know that repeat shoppers are some of the most valuable patrons to walk through their doors. But just how valuable was that new customer you just met? Or how profitable are your best and most loyal customers? To find out, we’re going to crunch some numbers so we can better understand the lifetime value of your customers.

The value of a new customer

The average small business spends about $400 a month on marketing. Since most of that money goes toward attracting new customers, let’s start by figuring out how much that new customer is actually worth.

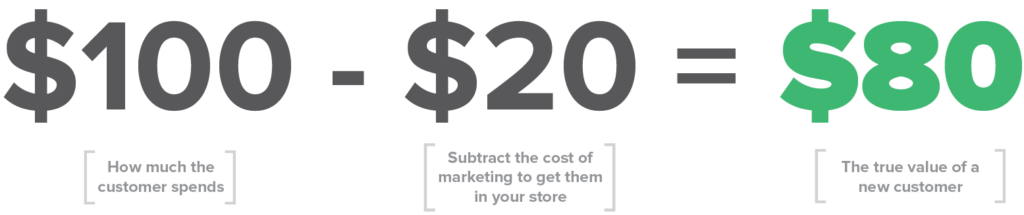

Calculating the initial value of a customer is quite simple. We take their first purchase, subtract the amount of your marketing budget that you spent to get them to your store, and you have a rough estimate of their initial value.

Let’s say you’re an independent retailer. The average customer spends about $100 at a time with local retailers. We subtract the cost of the marketing budget required to get them in your store. While this number varies from industry to industry, for many retailers the cost of a new customer ranges from $10-$30. For the sake of simplicity, we’re estimating the cost of a new customer to be about $20. So, in this example, we’d say this customer’s initial value was about $80.

Why calculate the initial value? By most estimates, 60-80% of satisfied customers don’t return for a second visit. So, while the lifetime value for a customer can often exceed 10 times their initial purchase, the vast majority of your customers will only visit your store once, unless you have a method or plan to re-engage them. If you’re in a different industry, if your customers spend less on average, or your cost to attract a new customer is higher, you can see how those factors add up and contribute to the lifetime value of your customer base.

The impact of repeat visits on a customer’s lifetime value

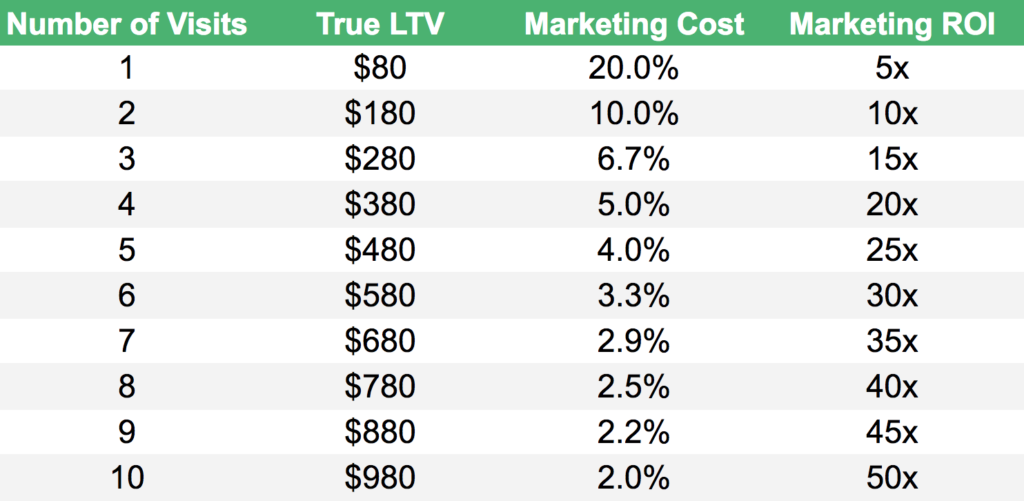

To calculate the lifetime value of a customer, we need to know how often they return. Below, you’ll find a basic chart that shows how your marketing spend maximizes with each return visit. The cost of marketing does down and lifetime value increases with every return visit by a customer.

In our initial purchase, we saw a 5x return on our marketing investment. That may sound pretty good, and for many businesses, seeing a 5x return on the first purchase would be quite significant. But the truth is that 20% of that customer’s purchase went back into the marketing budget.

It won’t come as a surprise to hear that repeat business is key to increasing revenue and profits. What may be more surprising is how quickly small business owners can maximize their marketing efforts by encouraging repeat business. By the time a customer comes back for the fourth time, their cost of marketing will have dropped from 20% to just 5%. Assuming they continue to spend what the average customer spends in your store, that’s a 20x return!

Why calculate the lifetime value? Business owners work on thin margins, and while most know that repeat business is one of the most important things they should be doing, only 18% of businesses focus on customer retention. Understanding a customer’s lifetime value helps realize the potential of every customer and empowers business owners to be more intelligent and deliberate with re-engagement and win-back strategies.

Why one-time buyers may be hurting your profits

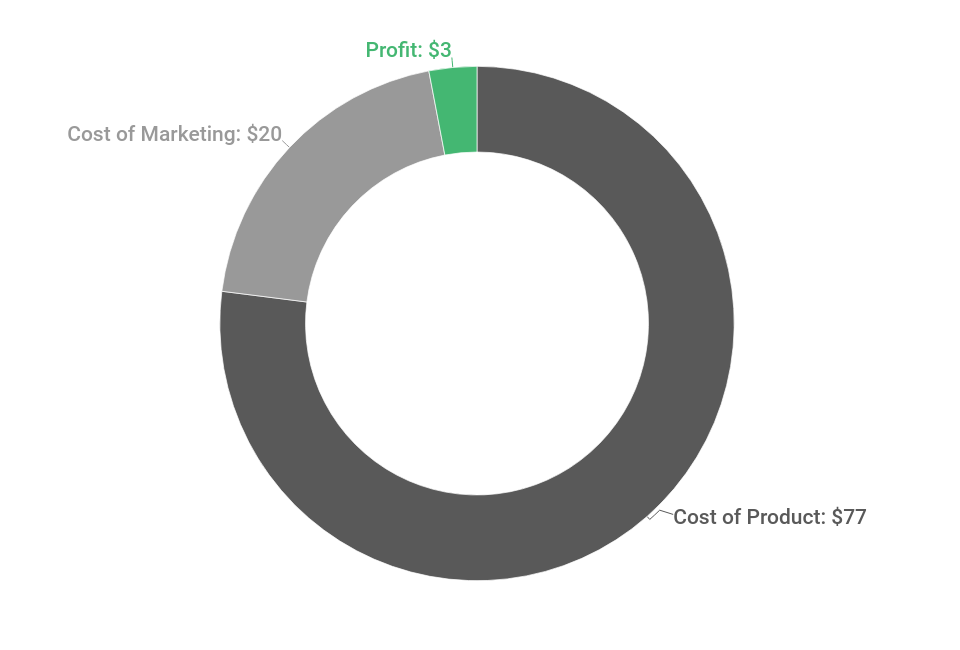

Let’s take things one step further. The average local retailer has about a 30% markup. In simple terms, when a customer spends $100 in a retailers store, they’re buying $77 worth of product and about $23 in markup.

Both rates are a bit fixed. The $23 profit margin is necessary for payroll, overhead, and business operations. That $77 is a fixed cost for businesses unless their supplier can sell them gear at a discounted wholesale price. Now factor in your marketing and the value of that new customers, you’ve only added about $3 in profit.

Now, every business needs to attract new customers, but you can’t stop there. If your business is mostly comprised of one-time buyers, you may struggle to increase your profit margins as you will constantly need to reinvest a large portion of each new customer’s purchase back into your marketing efforts. If you feel your profits are lagging, it would be worth looking into your customers average lifetime value.

Now, every business needs to attract new customers, but you can’t stop there. If your business is mostly comprised of one-time buyers, you may struggle to increase your profit margins as you will constantly need to reinvest a large portion of each new customer’s purchase back into your marketing efforts. If you feel your profits are lagging, it would be worth looking into your customers average lifetime value.

In this model, we used retail standards. But it’s not hard to imagine a situation where a business owner would spend more to attract a new customer than they often make in from that customer’s first purchase. If your margins aren’t as high, if your customers don’t spend as much with your business, or you’re in a different industry, you could see a negative impact on sales by focusing exclusively on attracting one-time customers.

Repeat business is key to increasing profits

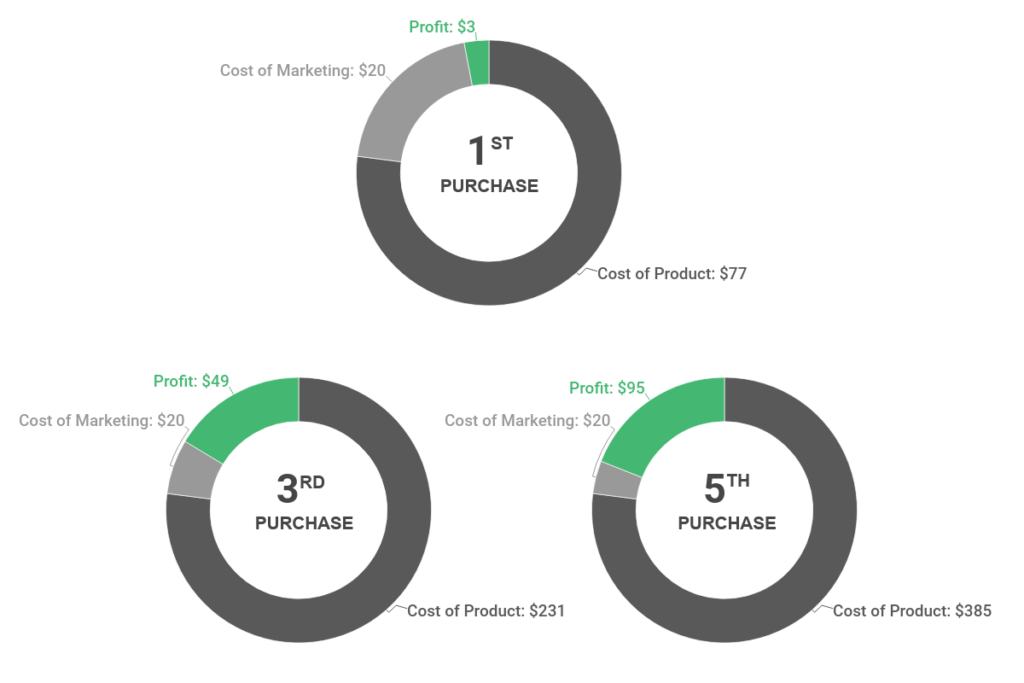

On the other hand, as we saw in the table above, repeat business can have a very positive impact on your bottom line. Below, we have another graph to show you how profits and the cost of marketing drastically change within just a few purchases.

You’ll notice the percentage of the marketing cost drops significantly from the first purchase to the fifth. Small business owners increase profits significantly with just a few repeat purchases. Getting a customer to return for a third purchase could increase profits more than acquiring 15 new customers who only visit once.

When you consider that it can be 5 to 25-times more expensive to attract a new customer than it is to encourage an existing customer to come back, having a customer retention strategy becomes a no-brainer. We can also see why a 5% increase in customer retention could increase profits upwards of 95%, according to The Harvard Business Review.

Take action

Encouraging customers to come back is much easier than many business owners think. For the most part, customers just need a gentle nudge to encourage them back and get them shopping in your store again. It may just take a simple reminder email.

See how Womply can help small businesses automate parts of their customer retention strategy. Learn more, plus get free reputation monitoring and customer insights when you sign up for Womply Free!